Sustainable Funds Markets: A Comparison of Europe and the USA

Katarzyna Domańska *

Tomasz Miziołek *

Keywords: sustainable investment trends, mutual funds, financial regulations

JEL: F65, G11, Q56

Rynki funduszy zrównoważonych: porównanie Europy i Stanów Zjednoczonych

Streszczenie: W ostatnich latach fundusze zrównoważone stały się jednym z najszybciej rozwijających się segmentów globalnego rynku funduszy inwestycyjnych. Zjawisko to jest szczególnie wyraźne w dwóch najbardziej rozwiniętych regionach świata – Stanach Zjednoczonych i Europie. Tempo ekspansji oraz warunki jej towarzyszące wykazują jednak istotne różnice pomiędzy tymi rynkami. Artykuł porównuje rozwój rynków funduszy zrównoważonych w USA i w Europie w latach 2020–2024, wskazując kluczowe czynniki determinujące obserwowane tendencje. Europa zdecydowanie wyprzedziła Stany Zjednoczone pod względem dynamiki wzrostu funduszy zrównoważonych, co wynika przede wszystkim z bardziej skutecznych ram prawnych, obejmujących standardy raportowania ESG oraz regulacje dotyczące inwestycji finansowych. Rynek europejski wykazał również większą odporność na zaburzenia gospodarcze i geopolityczne. W latach 2022–2024 nastroje inwestorów uległy pogorszeniu, co przełożyło się na spadek napływu kapitału do funduszy, wzrost liczby ich likwidacji, fuzji oraz procesów rebrandingu w obu regionach.

Słowa kluczowe: trendy inwestycji zrównoważonych, fundusze inwestycyjne, regulacje finansowe

1. Introduction

Growing social awareness of global challenges and increasing prominence of the sustainable development paradigm has prompted interest in investments that adhere to sustainability criteria (ESG – Environmental, Social, Governance). Therefore, sustainable investment funds incorporating these principles are becoming increasingly popular among investors who seek, alongside performance, a positive impact on the environment and society. The Morgan Stanley Institute for Sustainable Investing survey (2024) showed that 54% of individual investors intended to increase their sustainable investments in 2024, and 77% were interested in sustainable investing. Bioy et al. (2025a) reported that at the end of 2024, the global sustainable fund market reached USD 3.2 trillion.

According to Schoenmaker (2018), sustainable investment entails a “long-term investment approach, which integrates ESG factors into the research, analysis, and selection process of securities within an investment portfolio.” In this study, we adopt the Bioy et al. (2025a) approach and assume that the global sustainable fund universe encompasses open-end funds and exchange-traded funds that, through their prospectus or other regulatory filings, claim to focus on sustainability, impact, or environmental, social, and governance factors.

Notably, from a definitional standpoint, “sustainable funds” lack a single, universal definition across jurisdictions and data providers. Eurosif (2024) proposes a four-tier classification (Basic ESG, Advanced ESG, Impact-Aligned, and Impact-Generating), based on binding sustainability criteria across the investment process. GSIA’s Global Sustainable Investment Review uses a broad taxonomy (e.g., exclusionary/norms-based screening, ESG integration, thematic and impact investing, stewardship) that aggregates region-specific practices. By contrast, ESMA (2024) links the use of ESG/sustainability terms in fund names to quantitative thresholds under the EU’s SFDR regime, thereby anchoring definitions in enforceable disclosure rules. These methodological and regulatory divergences limit cross-market comparability and help explain discrepancies in the reported scale and performance of “sustainable” fund segments.

Even though the assets of sustainable funds worldwide exhibit an upward trend (Bioy et al. 2025a), market growth remains inconsistent between regions. Globally, sustainable fund assets were distributed with Europe at 84% of market share, while the U.S. held 11% at the end of December 2024 (Bioy et al. 2025a). The European market leads in sustainable investment funds, even though the U.S. holds 53.3% of global regulated open-end fund assets, compared with Europe’s 29.8% share in 2024 (EFAMA 2025).

This research investigates the sustainable fund market’s development across Europe and the U.S. from 2020 through 2024 by analyzing fund flows, total net assets, the number of funds, and fee levels. Given the rapid expansion of sustainable investing, especially in Europe, we examine the extent to which regulatory frameworks, investor preferences, and economic factors have influenced this growth. Our main goal is to identify the underlying structural differences between these two regions and assess their broader implications for investors, regulators, and other stakeholders.

2. Regulatory frameworks of sustainable funds

The sustainable investment landscape shows significant differences between Europe and the United States due to their legal and political systems. Soyombo et al. (2024) state that the differences in sustainability reporting between the United States and Europe are due to distinct regulatory frameworks, cultural factors, and stakeholder demands. The United States does not have mandatory ESG reporting laws, so practice is largely shaped by voluntary choices made by companies. By contrast, European companies must disclose sustainability issues through legal requirements, reflecting policy initiatives that seek to incorporate ESG principles into financial decision-making.

Singhania and Saini (2021) point out that the EU requires mandatory disclosure of non-financial information, a policy embraced by many member states. The EU’s ESG regulatory framework presents both challenges and opportunities for improvement. Frecautan and Nita (2022) also recognize its essential value as a strategic instrument for climate transition activities of companies, their employees, and consumers. EU policy supports sustainable investment practices and protects against greenwashing activities (European Parliament 2023). The main regulations for sustainable investments in the European Union are detailed in Table 1.

The EU has revised numerous investment regulations to include ESG criteria in its framework. The Alternative Investment Fund Managers Directive (AIFMD) and the Undertakings for Collective Investment in Transferable Securities (UCITS) Directive have been updated to include sustainability requirements that added ESG risk-management obligations and disclosure requirements (ESMA 2019). The Sustainable Finance Disclosure Regulation (SFDR) and Taxonomy Regulation receive enforcement support from European supervisory authorities, including the European Securities and Markets Authority (ESMA), the European Banking Authority (EBA), and the European Insurance and Occupational Pensions Authority (EIOPA). These authorities help connect regulatory goals with real-world operational capabilities. Regulatory technical standards (RTS) operationalize high-level rules into specific, enforceable requirements (ESMA 2019). Through their guidelines, financial institutions receive directions to properly execute the regulations.

| Regulation | Legal Act | Scope | Key Requirements |

|---|---|---|---|

| Sustainable Finance Disclosure Regulation (SFDR) |

Regulation (EU) 2019/2088 |

Financial market participants, investment funds, financial advisors |

Classifies funds into Article 6 (no ESG integration), Article 8 (‘light green’ – promotes ESG), and Article 9 (‘dark green’ – fully sustainable investments). Mandates ESG-related disclosures at both the entity and product levels. |

| EU Taxonomy Regulation |

Regulation (EU) 2020/852 |

Large companies, financial institutions, and investors marketing sustainable products |

Establishes six environmental objectives: climate change mitigation, climate change adaptation, sustainable water use, circular economy, pollution prevention, and biodiversity protection. Provides technical screening criteria for sustainable economic activities. |

| Corporate Sustainability Reporting Directive (CSRD) |

Directive (EU) 2022/2464 |

Large EU companies (250+ employees, €40M revenue, €20M assets) and listed SMEs |

Expands mandatory ESG disclosure obligations, requiring detailed reporting on environmental, social, and governance aspects in accordance with European Sustainability Reporting Standards (ESRS). |

| Markets in Financial Instruments Directive II (MiFID II) |

Directive 2014/65/EU |

Investment firms, financial advisors, asset managers |

Requires financial advisors to integrate clients’ ESG preferences into investment suitability assessments. Mandates ESG training for advisors to ensure informed client guidance. |

| Amendment to Delegated Regulation (EU) 2017/565 under MiFID II |

Regulation (EU) 2021/1253 |

Investment firms, portfolio managers, and financial advisors under MiFID II |

Amends MiFID II delegated acts to integrate clients’ sustainability preferences into the investment advisory and portfolio management processes. Requires firms to assess and document ESG preferences during client suitability assessments, and to offer financial instruments aligned with those preferences. |

| European Green Bond Standard (EUGBS) |

Regulation (EU) 2024/917 |

Issuers of green bonds within the EU |

Establishes a voluntary standard for green bonds aligned with the EU Taxonomy. Requires detailed reporting on the use of proceeds and external verification to enhance transparency and credibility in the green bond market. |

| EU Benchmark Regulation (EU BMR) – ESG Benchmarks |

Regulation (EU) 2019/2089 (amending EU BMR) |

Index providers and benchmark administrators offering ESG-related indices |

Introduces EU Climate Transition Benchmarks and EU Paris-Aligned Benchmarks. Ensures transparency in ESG benchmark methodologies and alignment with sustainability objectives. |

Source: Own elaboration.

The European Union promotes sustainable development, encouraging European countries outside the EU to harmonize their regulations with EU standards. In the United Kingdom, the Task Force on Climate-related Financial Disclosures (TCFD) Regulations (2022) enforce TCFD reporting, and the Financial Conduct Authority (2023) ensures transparency of sustainability claims. In Switzerland, 2024 regulations issued by the Federal Council oblige companies to disclose climate risks and face corporate accountability measures. Under the Norwegian Transparency Act, businesses must conduct supply-chain due diligence, and the Ministry encourages financial reporting to follow TCFD guidelines (Norwegian Ministry of Labor and Social Inclusion 2022). These efforts reflect Europe’s broader commitment to sustainable regulations.

The United States does not operate under a single framework that governs sustainable investing regulations. Rules and priorities differ between Democratic and Republican administrations. Party control shapes sustainable-investment rules and the broader regulatory environment. Laidler (2017) explains that Democrats usually back regulations that advance environmental sustainability and address climate change. The Republican Party often views such measures as financial restrictions, arguing that ESG factors should influence decisions only when they are financially material. Political polarization creates major challenges for the United States to establish and reach environmental sustainability targets (Akadiri, Alola 2020), posing obstacles to long-term, cohesive, and effective nature- and social-protection policies.

Liscow and Sunstein (2024) argue that regulatory frameworks under Democratic leadership focus on welfare and equity. The Enhancement and Standardization of Climate-Related Disclosures for Investors (Securities and Exchange Commission 2022), together with the Inflation Reduction Act (U.S. Congress 2022), were established under a Democratic administration. Regulatory agencies permitted fiduciaries to analyze ESG factors in retirement-plan investments as long as those factors were financially material (Employee Benefits Security Administration 2022). These regulations led businesses to disclose climate-risk information and helped drive sustainable-investment development.

By contrast, Republican administrations have taken a more restrictive approach. Numerous legal acts introduced under Republican control prioritize financial returns over sustainability considerations. The Financial Factors in Selecting Plan Investments Rule prohibited fiduciaries from considering ESG factors unless they could demonstrate a direct financial benefit (U.S. Department of Labor 2020). At the state level, Republican-led states such as Texas and Florida passed laws restricting state pension funds from incorporating ESG factors, arguing that such considerations introduce political biases into financial decision-making (Harvard Law School Forum on Corporate Governance 2023). As a consequence of these contradictory political aims, the U.S. legal framework for sustainable investments consists of both pro-ESG and anti-ESG acts. Table 2 summarizes the key sustainable-investment regulations in the U.S.

| Regulation | Legal Act | Scope | Key Requirements |

|---|---|---|---|

| Investment Company Act ESG Rule (‘Names Rule’) |

Amendments to Rule 35d-1 (2023) |

Investment funds registered under the Investment Company Act of 1940 |

Mandates that any fund using ESG-related terms in its fund name or marketing materials must allocate at least 80% of assets to investments that align with its stated ESG objectives. Requires clearer prospectus disclosures regarding ESG integration. |

| Department of Labor (DOL) ESG Rule under ERISA |

Prudence and Loyalty in Selecting Plan Investments and Exercising Shareholder Rights (2023) |

Private-sector retirement plans regulated under ERISA |

Allows fiduciaries of 401(k) and pension plans to consider ESG factors only when they are financially material to investment performance. Prohibits using ESG factors for non-financial objectives in retirement plan management. |

| Texas Anti-ESG Investment Law |

Senate Bill 13 (SB 13) (2021) |

Texas public pension funds & state investment agencies |

Bans state pension funds and agencies from investing in financial institutions that ‘boycott’ fossil fuel companies. Requires the Texas Comptroller to maintain a public list of restricted financial institutions. |

| Florida Anti-ESG Investment Law |

House Bill 3 (HB 3) (2023) |

State and local government investment entities |

Prohibits ESG factors from being used in state contracts, municipal bond issuance, and pension fund management. Mandates that all investment decisions be based exclusively on pecuniary financial returns. |

| Illinois Pro-ESG Investment Law |

House Bill 4812 (HB 4812) (2022) |

State pension funds in Illinois |

Requires state-managed retirement funds to develop and disclose an ESG integration strategy, report annually on their ESG investment approach, and consider climate risk assessments in portfolio management. |

Source: Own elaboration.

Singhania and Saini (2021) state that the USA has a less centralized approach to ESG regulation than the EU, with a mix of voluntary and mandatory disclosure practices. Camilleri (2015) states that the absence of a standardized regulatory framework in the USA has resulted in a diverse landscape of reporting methodologies. Companies tend to follow global standards like the Global Reporting Initiative (GRI) or industry-specific methodologies, as investor and consumer expectations demand so. Table 3 outlines the main differences in the ESG Regulations in Europe and the United States.

| Criteria | Europe | United States |

|---|---|---|

| Legal Approach |

Comprehensive, mandatory regulations at the EU level (SFDR, CSRD, Taxonomy Regulation, MiFID II). National rules (UK, Switzerland, Norway). |

Fragmented; varies by administration. No unified federal framework. State-level ESG restrictions exist in some Republican-led states. |

| Sustainability Taxonomy |

EU Taxonomy Regulation defines six environmental objectives for classifying sustainable activities. |

No federal taxonomy: sustainability definitions depend on voluntary standards and market-driven classifications (SASB, TCFD, GRI). |

| Investment Fund Classification |

SFDR categorizes funds into Article 6 (no ESG integration), Article 8 (promotes ESG), and Article 9 (fully sustainable). |

No official classification system: ESG labels are determined by fund managers and industry self-regulation. The SEC adopted amendments to the Names Rule, requiring funds with names suggesting specific characteristics (e.g., ESG) to invest at least 80% of their assets accordingly. |

| Corporate Sustainability Reporting |

CSRD mandates ESG disclosures for large and publicly listed SMEs. |

SEC (2022) proposed mandatory climate disclosures, but implementation is politically contested. Many firms voluntarily adopt GRI, SASB, or TCFD standards. |

| Financial Advisory Requirements |

MiFID II requires financial advisors to consider clients’ ESG preferences in investment advice. |

No federal requirement for financial advisors to consider ESG. Some advisory firms voluntarily integrate ESG into investment recommendations. |

| Climate Risk Disclosure |

Mandatory under CSRD and EU Taxonomy Regulation. National-level obligations exist in the UK, Switzerland, and Norway. |

SEC (2022) proposed climate-related disclosure rules, but enforcement depends on political landscape. Many companies follow TCFD voluntarily. |

| Regulatory Stability |

Stable, long-term framework at the EU level with evolving updates to enhance ESG integration. |

Highly volatile due to political polarization; regulations change between Democratic and Republican administrations. |

| Government Incentives for Sustainable Investment |

EU Green Deal and national-level initiatives support green investment through subsidies and financing mechanisms. |

Inflation Reduction Act (2022) provided financial incentives for clean energy and sustainable infrastructure investments. |

| Restrictions on ESG Integration | No restrictions: ESG integration is actively promoted by EU policies. | Republican-led states (e.g., Texas, Florida) restrict ESG investing in state pension funds. |

Source: Own elaboration.

3. Sustainable funds markets in Europe and the USA

This quantitative analysis of sustainable-fund market development in Europe and the U.S. between 2020 and 2024 examines four elements: capital flows, assets, the number of funds, and cost structures. Regarding the first three, the research follows the Morningstar methodology and includes open-end funds (OEFs) and exchange-traded funds (ETFs) that use ESG criteria for security selection and demonstrate a sustainability theme or aim to create a measurable positive social impact alongside financial performance (Bioy et al. 2020).

According to Morningstar’s methodology, the global sustainable fund universe encompasses OEFs and ETFs that, by prospectus or other regulatory filings, claim to focus on sustainability, impact, or environmental, social, and governance factors. This universe is based on intentionality. Morningstar identifies intentionality using a combination of fund names and information detailed in fund documents, which should contain enough detail to make clear that ESG issues play an important role in security selection and portfolio construction. The global sustainable fund universe contains neither funds referred to as “ESG-integrated funds” (which do not make ESG considerations the focus of the investment process) nor funds that employ limited exclusionary screens such as controversial weapons, tobacco, and thermal coal (whether combined with an ESG-integration approach or not). Meanwhile, it includes ESG-screened passive funds, since exclusions are typically the sole purpose of their strategy (Bioy et al. 2025b). Because this methodology is not based on any particular regulatory framework, it differs significantly from the EU’s SFDR, which defines “sustainable investments” at the holdings level.

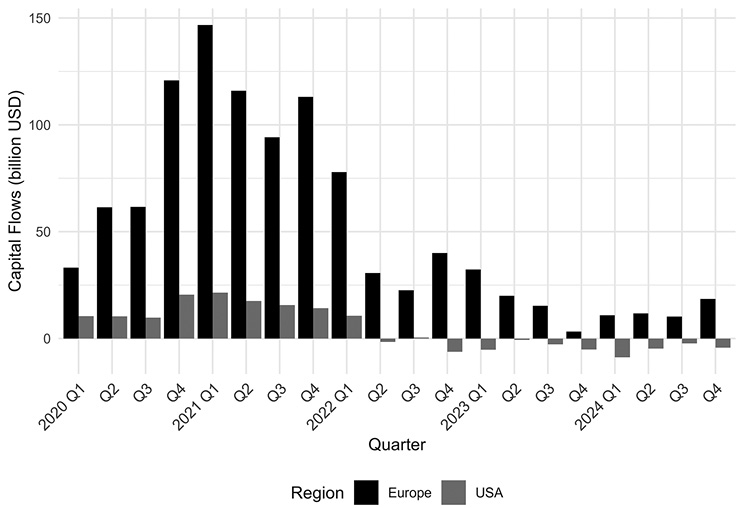

European- and U.S.-domiciled sustainable funds attracted USD 1.13 trillion in net capital inflows during the five years, showing strong investor interest in these products. The majority of this capital (92%) went to European-domiciled funds, which received USD 1.04 trillion. Notably, the European market received positive capital inflows during all five years under evaluation. The largest capital inflows occurred during 2021 (USD 470 billion), and 2022 brought USD 277 billion.

The COVID-19 pandemic created financial-market instability in 2020; however, ESG interest surged, supported by new regulations and studies suggesting that companies with stronger ESG profiles outperformed during downturns. This led to substantial investment inflows in the last quarter of 2020 and throughout 2021, with quarterly inflows exceeding USD 100 billion (Bioy et al. 2021). Sustainable funds continued to receive capital at a stable rate despite harsh conditions in equity and fixed-income markets during 2022. The subsequent two years saw net sales decline substantially; however, they remained positive. The decrease in sales stemmed from inconsistent fund performance, greenwashing concerns, geopolitical and regulatory uncertainties, and rising opposition to ESG in the U.S.

Source: Own elaboration based on Morningstar Reports.

In 2022, the European sustainable-investment market experienced a significant shift toward passive sustainable funds, as investors favored index-tracking strategies primarily for cost efficiency. The market preference for passive sustainable funds became most pronounced during 2023 and 2024, when these funds received USD 142 billion while active sustainable funds lost USD 12 billion (Bioy et al. 2025a). Demand for sustainable products remained strong in 2022–2023, even as conventional funds experienced EUR 266 billion in net outflows (ALFI 2024).

Net flows into U.S. sustainable funds peaked in the first quarter of 2021 and have been steadily declining since then. Over the analyzed period, significant purchases were observed mainly in 2020 and 2021, with total inflows amounting to USD 120 billion. Although net inflows in 2022 were close to zero, this was relatively positive given that the overall U.S. fund market experienced USD 370 billion of outflows that year (Bioy et al. 2023). In the following two years, U.S. sustainable funds faced multiple headwinds: average returns lagged conventional peers, political tensions surrounding ESG continued, and concerns about greenwashing remained unresolved. Further complicated by state-level actions restricting the use of ESG criteria in investment decisions, these factors prompted many investors to withdraw from such funds. As a result, total redemptions reached USD 34 billion in 2023–2024. This trend contrasts with the strong demand for long-term U.S. mutual funds and ETFs, which received a combined USD 721 billion in net inflows in 2024. Despite shifting sentiment, passive funds consistently outperformed their active counterparts in terms of net flows. Index-tracking sustainable products received more capital from 2020 to 2022 and experienced reduced outflows in 2024 compared with actively managed funds, with 2023 the only exception.

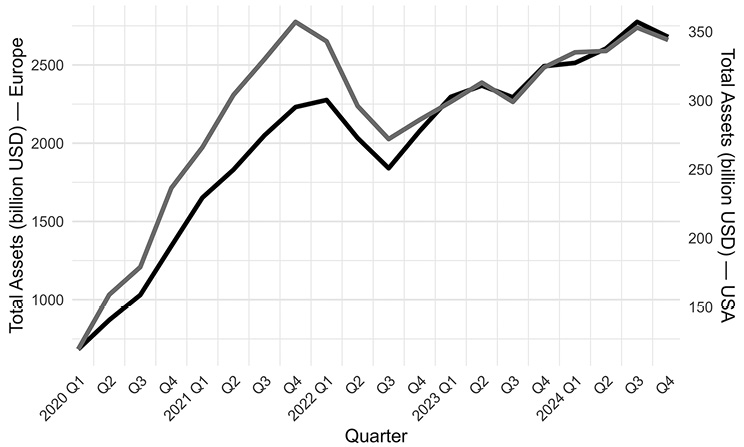

The substantial difference between European-domiciled and U.S. sustainable funds is reflected in their assets under management (AUM). At the end of 2024, European sustainable funds managed USD 2.68 trillion in assets, while U.S. sustainable funds managed USD 0.34 trillion. European funds held the largest share of global sustainable-fund assets, accounting for 81–85% during 2020–2024 (average 82.8%), while U.S. funds held 10–15% (average 12.3%). European sustainable funds achieved a compound quarterly growth rate (CQGR) of 7.5%, while U.S. sustainable funds experienced a CQGR of 5.7%. Funds in the rest of the world (Asia, Canada, Australia, New Zealand) accounted for only 5.1% of total AUM at the end of 2024 (USD 163 billion).

Even though, based on the MSCI Europe and MSCI USA indexes, European equity returns were lower in 2020–2021 and 2023–2024, European sustainable-fund assets still grew faster than in the U.S. Despite adverse market conditions, European sustainable funds expanded their dominance over their U.S. counterparts, primarily due to strong regional demand for sustainable products. During 2020–2021, the U.S. sustainable-fund market’s largest growth came mainly from rising stock-market values rather than new investor contributions. In the subsequent three years, U.S. sustainable-fund assets failed to surpass their end-2021 peak; the 2023–2024 equity rally proved insufficient to offset persistent outflows.

By the end of 2023, the sustainable-funds sector accounted for about 19% of European fund assets – higher within equity funds. According to EFAMA (2024), the share of net assets of sustainable equity UCITS in total equity UCITS assets in Europe increased from 19% to 23% in 2019–2023. In contrast, the U.S. maintained its sustainable-fund market share at less than 1% (ALFI 2024). The European sustainable-fund market is less concentrated than in the U.S.: at the end of 2024, the top five managers in Europe (BlackRock, UBS, Amundi, Swisscanto, DWS) accounted for 34.2% of total net assets, whereas in the U.S. the top five (BlackRock, Vanguard, Parnassus, Morgan Stanley, Nuveen) held 56.4% (Bioy et al. 2025a).

In terms of management style, both regions display a similar AUM mix: active strategies remain dominant. In Europe, roughly two-thirds of sustainable AUM (about USD 1.8 trillion) are actively managed; in the U.S., about 60% (about USD 0.2 trillion) are active (Bioy et al. 2025c). At the same time, flow data indicates a persistent rotation toward lower-cost, index-based vehicles, steadily lifting the passive ESG share.

Although the secular shift toward sustainable ETFs – predominantly passive instruments (approximately 91%) – continues to accelerate, these funds still represent a minority share of total assets in both regions: around 19% (USD 0.45 trillion) in Europe and around 23% (USD 0.07 trillion) in North America as of end-2024 (ISS 2025). Nevertheless, the dynamic global expansion of passive instruments, particularly ETFs, highlights the growing appeal of index-based strategies within the sustainable-funds segment.

The most pronounced growth can be observed in European markets, where the development of insurance companies and pension funds constitutes a key driver of ESG-ETF asset accumulation. Beyond purely financial factors, several structural and institutional determinants also play an important role in Europe, including the level of stock-market development, the degree of ICT adoption, financial access and literacy, and the prevalence of tertiary education. By contrast, the influence of sustainable-fund performance and taxation levels appears relatively limited (Marszk, Lechman 2024). These factors help explain why sustainable funds continue to attract investors in Europe even when their performance lags conventional or partially sustainable funds. Empirical evidence supports this observation: Bosio et al. (2025) examine 9,620 mutual funds distributed in Europe between October 2018 and January 2025 and find that Article 9 funds significantly underperformed both Article 6 and Article 8 funds.

Source: Own elaboration based on Morningstar Reports.

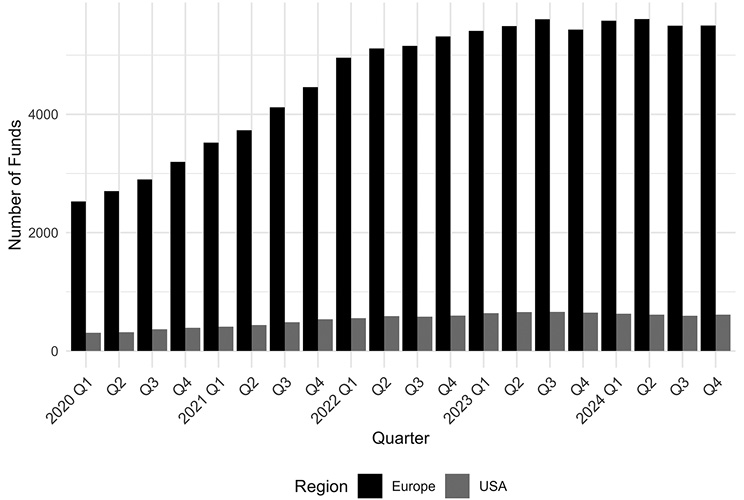

A similar discrepancy to that observed in capital flows and assets under management is also evident in the statistics concerning the number of sustainable funds and the pace of product development. The total number of sustainable funds in Europe maintained a 90 percent share of the combined market during 2020 through 2024, despite all legal and economic changes in the broader environment. The European sustainable fund numbers experienced continuous growth between 2020 and 2024 at a compound quarterly rate of 4.2 percent.

An important feature of the European market is that most ETFs, including sustainable ones, are cross-listed, which means that their shares (units) trade simultaneously on more than one stock exchange. Frequently, a fund that is fundamentally identical in terms of exposure and costs is offered as a separate instrument on different exchanges, often with varying share classes or trading currencies (Marszk, Lechman 2019). According to PwC (2024), 38.3% of European ETFs have two-three listings, and another 26.8% have four or more. Consequently, the headline number of sustainable ETFs in Europe is, to some extent, inflated by the absence of a single unified market such as in the U.S.

Two primary factors behind this growth were the launch of new sustainable investment funds and the transformation of existing conventional funds into sustainable ones. The European market experienced rapid new fund launches throughout 2020 and 2021. Asset management companies launched complete sustainable fund families during 2020 and 2021 because investors showed an increasing interest in sustainable investments (see Figure 3).

Source: Own elaboration based on Morningstar Reports.

New launches and repurposing weakened markedly over the past three years, with a pronounced slowdown in 2024. Managers shifted toward a “quality over quantity” approach, emphasizing differentiation (Bioy et al. 2025a). Regulatory momentum intensified with ESMA’s (2024) guidelines on the use of ESG- and sustainability-related terms in fund names. Against persistent greenwashing allegations, leading managers such as BlackRock, DWS, BNP Paribas, UBS, and State Street Global Advisors responded by renaming funds or adjusting investment approaches to meet the new standards (Gordon 2025). Following the May 2024 release of the ESMA guidelines, the European market recorded a 20% decline in sustainability-named funds (Gangadia 2025). Collectively, these developments produced a notable deceleration in the growth of ESG-labeled funds in recent quarters, with some periods registering negative growth.

At the end of the period, the U.S. sustainable-fund market remained much smaller than Europe’s, with 612 registered products versus 5,502 in Europe, and it also exhibited less product variety. However, this asymmetry reflects structural differences rather than a simple gap in “development.” Europe’s market is more complex and fragmented owing to heterogeneous regulation and investor behavior. European investors have long favored locally domiciled products; combined with jurisdiction-specific rules, this preference encourages vehicles tailored to national markets, often duplicating similar approaches. By contrast, the U.S. market’s centralization supports fewer funds with wider distribution and scalability.

Rising investor demand drove substantial product development in the U.S. between 2020 and 2022, when the market added over 100 sustainable funds per year, compared with about 50 per year in 2015–2019. Most were new launches; only a small share reflected reclassifications. Momentum reversed in the second half of 2023 as investor interest waned, and the downturn persisted through 2024. New launches fell sharply from mid-2023, with only a handful introduced each quarter; in total, the U.S. saw just 10 new sustainable funds in 2024.

Closures followed a different trajectory. Before 2022, shuttering sustainable funds was rare. Starting in 2023, however, managers began reducing sustain-able-fund line-ups as interest declined. Closures were accompanied by mergers and removals of sustainability mandates. Affected strategies included broad ESG, low-carbon equity, net-zero transition, energy transition, gender equality, and ocean health. Some liquidated funds had previously been repositioned but failed to secure durable inflows. The U.S. recorded more closures than launches beginning in Q4 2023 (Bioy et al. 2025a).

Another difference between European and U.S. markets lies in fee levels. ESMA (2025) reports that in 2023 the average total expense ratio (TER) for retail ESG UCITS funds in Europe was 1.1%. On average, ongoing costs of ESG funds were similar to those of non-ESG funds, although the asset-weighted costs of ESG funds were higher until 2021. Initial subscription fees for ESG funds were higher, at 2.3%, and redemption fees were also higher, by 2.2 percentage points, than those of conventional funds. From 2019 to 2023, the expense ratio of ESG funds consistently exceeded that of non-ESG funds. The average ongoing expenses for ESG funds reached 1.2%, versus 1.1% for non-ESG funds. One-off fees were 0.6% for ESG funds and 0.5% for non-ESG funds. Morningstar research shows a cost advantage for ESG funds in Europe: the asset-weighted average cost was 0.83% for ESG funds and 0.90% for non-ESG funds across six major categories (Wang et al. 2024). Fees have declined steadily over the years: average 2024 fees were 47% lower than in 2013. ESMA (2022) also finds that ESG funds tend to invest in larger companies and focus on developed markets more than non-ESG funds, which helps explain lower ongoing costs.

In the U.S., the asset-weighted average net expense ratio of sustainable funds was 0.52% in Q4 2023. This ratio reflects the share of assets that goes toward operating and management expenses (including 12b-1 fees and administrative costs), excluding brokerage costs and sales loads. Average asset-weighted fees for U.S. sustainable funds decreased by 44% over the last decade, driven by numerous low-cost sustainable index mutual funds and ETFs that attracted significant inflows (Evens, Armour 2024).

Similarly, U.S. sustainable funds have slightly lower expenses than non-ESG funds. Black and Kölbel (2024) show that, controlling for fund characteristics, U.S. ESG funds charged net expense ratios 9.5–12.7 basis points lower than non-ESG funds over 2011–2024. The cost advantage started in 2015 and remained statistically significant through 2024. However, gross expense ratios were higher for ESG funds because they include full operating and distribution costs before fee waivers or reimbursements. Some asset managers use fee reductions for ESG funds as a marketing tactic to offset concerns about performance. Because ESG funds often maintain portfolios similar to conventional peers, competition within the ESG segment has intensified. Managers sometimes pursue cross-selling, using ESG funds to attract new investors who may later be directed toward higher-cost products in the same family. Current market conditions mean investors choosing sustainable funds do not face a “greenium,” as fees are not higher than for conventional funds.

4. Conclusion

Europe and the United States represent two most significant markets for sustainable funds globally. Together, they account for approximately 95% of global AUM in this category and around 80% of the total number of sustainable funds as of end-2024. However, sustainable investing is a segment where Europe maintains market dominance compared with the conventional U.S. leadership in global investment funds. Europe leads through superior net inflows, larger AUM, and broader product offerings.

These two markets differ substantially because Europe implements stronger regulations and its population demonstrates greater enthusiasm for sustainable development. The institutional structure of sustainable finance diverges meaningfully between Europe and the U.S. European countries began pursuing the UN Sustainable Development Goals through national-level actions in the late twentieth century, followed by systematic advances within the EU framework. These provisions – particularly for sustainable financial products – emerged from a deep commitment to sustainable development. Europe’s asset-management sector adopted sustainable practices earlier and at larger scale than in the U.S., supported by investors with greater awareness of environmental and social impacts.

Interest in sustainable products had been rising over the previous decade, but 2020 was a defining moment that transformed sustainable-fund markets in both regions. The COVID-19 shock underscored the need for rapid adoption of sustainable practices across operations and investment approaches. Sustainable funds received intense inflows throughout 2020–2021. In Europe, legislative measures such as SFDR and the EU Taxonomy further boosted demand.

In contrast, U.S. sustainable funds also saw a rising interest, albeit from a lower base. Greenwashing concerns and political opposition to ESG limited adoption, with several states passing anti-ESG measures that created a less favorable regulatory environment than in Europe.

Despite differences, both markets faced similar macro and political headwinds. In 2022 – amid higher inflation, rising rates, recession fears, and Russia’s invasion of Ukraine – European sustainable funds proved resilient, maintaining substantial inflows. U.S. sustainable funds, by contrast, posted their first net outflow of the decade. In Europe, demand for low-cost passive products – especially ETFs – helped limit outflows, but this stability coincided with record numbers of closures, mergers, and rebranding. Many managers reacted to evolving regulatory expectations and reputational risks by removing or altering ESG-related terminology in fund names and strategies.

Although the European and U.S. markets differ in structural, regulatory, and cultural dimensions, they share broader arcs over the past five years: rapid early growth with significant inflows and product launches, followed by moderation as the segment matured and macro conditions shifted. As competition increased and demand moderated, only products delivering on performance and meeting investors’ needs persisted.

In summary, dynamics in both regions is driven by regulation, investor preferences, and product design – but constrained by divergent definitions of “sustainability.” The lack of a universal taxonomy across Eurosif, GSIA, and ESMA limits cross-market comparability and complicates performance assessment. For investors, due diligence on the methodological underpinnings of ESG labels and data sources is essential to manage classification risk, evaluate performance, and mitigate greenwashing exposure. For policymakers and regulators, the results highlight the need for international coordination and convergence of disclosure standards to improve comparability, credibility, and investor protection.

The study’s main limitation lies in its reliance on Morningstar data which, although widely adopted by institutions such as the OECD, the World Bank, and leading financial-research firms, is not universally used. Divergent frameworks developed by Eurosif, GSIA, MSCI, and ESMA use different inclusion criteria and sustainability taxonomies, which may introduce definitional and selection biases. Future research should integrate multiple data providers and methodological approaches to capture the heterogeneity of sustainable-investment practices across jurisdictions. Expanding the analysis to include emerging markets, fund-level ESG metrics, and longitudinal performance effects would provide a more comprehensive understanding of the global evolution of sustainable finance and its regulatory implications.

Autorzy

* Katarzyna Domańska

* Tomasz Miziołek

References

Akadiri S., Alola A. (2020), The role of partisan conflict in environmental sustainability targets of the United States, “Environmental Science and Pollution Research”, 27: 10265–10274, https://doi.org/10.1007/s11356-019-07174-8

ALFI (2024), European Sustainable Investment Funds Study 2024. Sustainable Investing Fuelling Resilient Growth for the Future, https://www.alfi.lu/en-gb/pages/setting-up-in-luxembourg/responsible-investing/european-sustainable-investment-funds-study-2024

Bioy H., Jmili S., Petit A., Boyadzhiev D., Stankiewicz A., Tam I., Hall E., Sato H., Seyunghye Jung A., Chow W. (2022), Global Sustainable Fund Flows: Q4 2021 in Review. Flows and assets continue to grow at the end of a landmark year, https://www.morningstar.com/lp/global-esg-flows

Bioy H., Pucci N., Stewart L., Carabia A. (2025c), US Sustainable Funds Landscape 2024 in Review, https://www.morningstar.com/lp/sustainable-funds-landscape-report

Bioy H., Stuart E., Boyadzhiev D., Petit A., Alladi A. (2021). European Sustainable Funds Landscape: 2020 in Review. A Year of Broken Records Heralding a New Era for Sustainable Investing in Europe, https://www.morningstar.com/en-uk/lp/sustainable-funds-landscape

Bioy H., Stuart E., Hale J., Tam I., Kennaway G., Sato H., Seyunghye Jung A. (2020), Global Sustainable Fund Flows. ESG funds show resilience during COVID-19 sell-off, https://www.morningstar.com/lp/global-esg-flows

Bioy H., Wang B., Carabia A., Lennkvist A., Popat S., Beaudoin H., Mizuta R. (2025b), Global Sustainable Fund Flows: Q1 2025 in Review. Record-high outflows amid new geopolitical challenges and an intensifying ESG backlash, https://www.morningstar.com/business/insights/research/global-esg-flows

Bioy H., Wang B., Pettit A., Stankiewicz A., Mohamed A., Hall E., Sato H., Seunghye Jung A., Beaudoin H. (2023), Global Sustainable Fund Flows: Q4 2022 in Review. European investors show continued appetite for ESG products despite headwinds, while U.S. investors retreat, https://www.morningstar.com/lp/global-esg-flows

Bioy H., Wang B., Pucci N., Carabia A., Popat S., Beaudoin H., Mizuta R., Biddappa A.R. (2025a), Global Sustainable Fund Flows: Q4 2024 in Review, https://www.morningstar.com/lp/global-esg-flows

Black A., Kölbel J. (2024), The Puzzle of ESG Fund Fees. Swiss Finance Institute, N° 24-109, https://www.sfi.ch/en/publications/n-24-109-the-puzzle-of-esg-fund-fees, https://doi.org/10.2139/ssrn.5053459

Bosio A.O., Giudici G., Taglialatela J. (2025). “Sustainable” Versus “Traditional” Mutual Funds: Is There Really a Difference? A Comparative Analysis Within the EU SFDR Classification Framework. Business Strategy and Development, https://doi.org/10.1002/bse.70083

BVI (2020), How far is the sustainable fund market in Europe? On the Competitive Position of the German Asset Management Industry, https://www.bvi.de/uploads/tx_bvibcenter/2020_European_Sustainable_Fund_Market_02.pdf

California Legislature (2023), Senate Bill 253 & Senate Bill 261 (SB 253 & SB 261), 2023–2024 Session, https://leginfo.legislature.ca.gov

Camilleri M. (2015), Environmental, Social and Governance Disclosures in Europe, “Sustainability Accounting, Management and Policy Journal”, 6: 224–242, https://doi.org/10.1108/SAMPJ-10-2014-0065

EFAMA (2024), Sustainable equity UCITS. Promoting sustainable business models, https://www.efama.org/sites/default/files/files/market-insights-18-sustainable-equity-ucits.pdf

EFAMA (2025), Worldwide Regulated Open-end Fund Assets and Flows. Trends in the Fourth Quarter of 2024, https://www.efama.org/sites/default/files/international-statistical-release-q4-2024.pdf

Employee Benefits Security Administration (2022), Prudence and loyalty in selecting plan investments and exercising shareholder rights, “Federal Register”, 87(230): 73822–73885, https://www.federalregister.gov/documents/2022/12/01/2022-25783/prudence-and-loyalty-in-selecting-plan-investments-and-exercising-shareholder-rights

ESMA (2019), Final report on integrating sustainability risks and factors in the UCITS Directive and the AIFMD, https://www.esma.europa.eu/sites/default/files/library/esma34-45-688_final_report_on_integrating_sustainability_risks_and_factors_in_the_ucits_directive_and_the_aifmd.pdf

ESMA (2022), The drivers of the costs and performance of ESG funds, https://www.esma.europa.eu/sites/default/files/library/esma_50-165-2146_drivers_of_costs_and_performance_of_esg_funds.pdf

ESMA (2024), Final Report: Guidelines on funds’ names using ESG or sustainability-related terms (ESMA34-472-440).

ESMA (2024), Guidelines on funds’ names using ESG or sustainability-related terms. ESMA34-1592494965-657, https://www.esma.europa.eu/sites/default/files/2024-08/ESMA34-1592494965-657_Guidelines_on_funds_names_using_ESG_or_sustainability_related_terms.pdf

ESMA (2025), Costs and Performance of EU Retail Investment Products 2024, https://www.esma.europa.eu/sites/default/files/2025-01/ESMA50-524821-3525_ESMA_Market_Report_-_Costs_and_Performance_of_EU_Retail_Investment_Products.pdf

European Commission (2020), Regulation (EU) 2020/852 on the Establishment of a Framework to Facilitate Sustainable Investment (EU Taxonomy Regulation), https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32020R0852

European Commission (2021), Commission Delegated Regulation (EU) 2021/1253 of 21 April 2021 amending Delegated Regulation (EU) 2017/565 as regards the integration of sustainability factors, risks and preferences into certain organizational requirements and operating conditions for investment firms, Official Journal of the European Union, L 277, 1–7, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32021R1253

European Parliament (2023), Transparency and Integrity of Environmental, Social, and Governance Rating Activities, https://www.europarl.europa.eu/RegData/etudes/BRIE/2023/753185/EPRS_BRI(2023)753185_EN.pdf

European Parliament and Council (2019), Regulation (EU) 2019/2088 on Sustainability‐Related Disclosures in the Financial Services Sector (SFDR), https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32019R2088

European Parliament and Council (2022), Directive (EU) 2022/2464 on Corporate Sustainability Reporting (CSRD), https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32022L2464

European Parliament and Council of the European Union (2019), Regulation (EU) 2019/2088 on sustainability‐related disclosures in the financial services sector (SFDR), Article 2(17), Official Journal of the European Union, L 317/1, https://eur-lex.europa.eu/eli/reg/2019/2088

Eurosif (2024), Methodology for Eurosif Market Studies on Sustainability-Related Investments, https://www.eurosif.org/wp-content/uploads/2024/02/2024.02.15-Final-Report-Eurosif-Classification_2024.pdf

Evens Z., Armour B. (2024), 2023 US Fund Fee Study, https://www.morningstar.com/lp/annual-us-fund-fee-study

Financial Conduct Authority (2023), PS23/16: Sustainability Disclosure Requirements (SDR) and investment labels, https://www.fca.org.uk/publications/policy-statements/ps23-16-sustainability-disclosure-requirements-investment-labels

Florida Legislature (2023), House Bill 3 (HB 3), 2023 Regular Session, https://www.flsenate.gov

Frecautan I., Nita A. (2022), Who is Going to Win: The EU ESG Regulation or the Rest of the World? – A Critical Review, The Annals of the University of Oradea. Economic Sciences, https://doi.org/10.47535/1991auoes31(2)011

Gangadia K. (2025), Evolution of Fund Naming Calls for Deeper, Data-Driven Sustainability Insights, https://www.msci.com/www/quick-take/evolution-of-fund-naming-calls/05427906358

Gordon J. (2025), BlackRock removes ‘ESG’ from 56 ETFs and funds housing $51bn, https://www.etfstream.com/articles/blackrock-removes-esg-from-56-etfs-and-funds-housing-usd51bn?utm_source=ActiveCampaign&utm_medium=email&utm_content=BlackRock%20removes%20%20ESG%20%20from%2056%20ETFs%20and%20funds%20housing%20%2451bn&utm_campaign=ETF%20Bulletin%2018%2F03%2F25

GSIA (2023), Global Sustainable Investment Review 2022, https://www.gsi-alliance.org/wp-content/uploads/2023/12/GSIA-Report-2022.pdf

Harvard Law School Forum on Corporate Governance (2023, March 11), ESG battlegrounds: How the states are shaping the regulatory landscape in the U.S., https://corpgov.law.harvard.edu/2023/03/11/esg-battlegrounds-how-the-states-are-shaping-the-regulatory-landscape-in-the-u-s/

Illinois General Assembly (2022), House Bill 4812 (HB 4812), 102nd General Assembly, https://www.ilga.gov

ISS (2025), 2024 Sustainable Fund Trends: Index ETFs Are the Silver Lining, https://insights.issgovernance.com/posts/2024-sustainable-fund-trends-index-etfs-are-the-silver-lining/

Laidler P. (2017), Does The U.S. Campaign Finance System Favor Republicans. Political preferences, pp. 115–136, https://doi.org/10.6084/M9.FIGSHARE.5216203

Liscow Z., Sunstein C. (2024), Efficiency vs. Welfare in Benefit–Cost Analysis: The Case of Government Funding, “Journal of Benefit-Cost Analysis”, https://doi.org/10.1017/bca.2024.22

Marszk A., Lechman E. (2019), Exchange-Traded Funds in Europe. Academic Press, https://doi.org/10.1016/B978-0-12-813639-3.00003-1

Marszk A., Lechman E. (2024), What drives sustainable investing? Adoption determinants of sustainable investing exchange-traded funds in Europe, “Structural Change and Economic Dynamics”, 69: 63–82, https://doi.org/10.1016/j.strueco.2023.11.018

Morgan Stanley Institute for Sustainable Investing (2024), Sustainable Signals: Understanding Individual Investors’ Interests and Priorities, https://www.morganstanley.com/content/dam/msdotcom/en/assets/pdfs/MSInstituteforSustainableInvesting-SustainableSignals-Individuals-2024.pdf

Norwegian Ministry of Labour and Social Inclusion (2022), Transparency Act, https://www.regjeringen.no/en/dokumenter/transparency-act/id2877319/

PwC (2024), European ETF Listing and Distribution 2024, https://www.pwc.lu/en/asset-management/docs/pwc-european-etf-listing-distribution.pdf

Securities and Exchange Commission (2022), The enhancement and standardization of climate-related disclosures for investors, “Federal Register”, 87(70): 21334–21473, https://www.federalregister.gov/documents/2022/03/28/2022-06224/the-enhancement-and-standardization-of-climate-related-disclosures-for-investors

Singhania M., Saini N. (2021), Quantification of ESG Regulations: A Cross-Country Benchmarking Analysis, “Vision: The Journal of Business Perspective”, 26: 163–171, https://doi.org/10.1177/09722629211054173

Soyombo O., Odunaiya O., Okoli C., Usiagu G., Ekemezie I. (2024), Sustainability reporting in corporations: A comparative review of practices in the USA and Europe. GSC Advanced Research and Reviews, https://doi.org/10.30574/gscarr.2024.18.2.061

State-Level Legislation: Texas Legislature (2021), Senate Bill 13 (SB 13), 87th Legislature, https://capitol.texas.gov

Swiss Federal Council (2024), Ordinance on Climate Disclosures, https://www.admin.ch/gov/en/start/documentation/media-releases.msg-id-92310.html

The Companies (Strategic Report) (Climate-related Financial Disclosure) Regulations 2022, SI 2022/31 (2022), https://www.legislation.gov.uk/uksi/2022/31/contents/made

U.S. Congress (2022), Inflation Reduction Act of 2022. Public Law No. 117-169, https://www.congress.gov/bill/117th-congress/house-bill/5376

U.S. Department of Labor (2020), Financial factors in selecting plan investments rule. “Federal Register”, 85(223): 72846–72878, https://www.federalregister.gov/documents/2020/11/13/2020-24515/financial-factors-in-selecting-plan-investments

U.S. Department of Labor (2023, January 30), Prudence and loyalty in selecting plan investments and exercising shareholder rights (Final Rule), “Federal Register”, https://www.dol.gov/agencies/ebsa/laws-and-regulations

U.S. Securities and Exchange Commission (2023, September 1), Amendments to Investment Company Act Rule 35d-1; Names Rule (Final Rule), “Federal Register”, https://www.sec.gov/rules/final

U.S. Securities and Exchange Commission (2024, March 20), The enhancement and standardization of climate-related disclosures for investors (Final Rule), “Federal Register”, https://www.sec.gov/rules/final

Wang B., Bioy H., Möttölä M. (2024), ESG Fund Fees. Myth busting: ESG funds aren’t more expensive than non-ESG funds, https://www.morningstar.com/lp/esg-fund-fees